Independent Contractor FAQs

What to Expect as an Independent Contractor

As a therapist or educator placed through Therapy Source, you’ll work as an independent contractor (1099 employee). As an Independent Contractor, you’ll experience the flexibility to select positions and hours that fit your life and schedule. You’ll also earn – on average – up to forty percent more than you would as a W2 employee in the same role. However, you’ll be responsible for securing your own health insurance, investing for retirement and paying income taxes.

Not sure where to start? We’ve put together some helpful information.

Table of Contents

How To Find Health Insurance

We understand that finding quality–and affordable–health insurance is important to independent contractors. The good news is that there are several options to choose from.

Affordable Care Act (ACA)

Independent contractors can enroll in quality health insurance plans through their state’s Health Insurance Marketplace or the government-sponsored Health Insurance Marketplace. Created in 2014, it offers four “metal categories”: Bronze, Silver, Gold, and Platinum.

Open enrollment for the ACA plans usually starts in November and end in mid-December. Health insurance plans bought by mid-December start on January 1 of the following year. However, life circumstances (such as a change in job) make it possible to qualify for special enrollment after open enrollment has already passed.

Freelancers Union

A superb resource for helping you learn more about health insurance terms, Freelancers Union is the largest organization representing 57 million independent workers and contractors nationwide. Based in New York City, Freelancers Union members have access to a full-service community, policy advocacy, and a benefits plan including retirement, health coverage, and dental insurance. Membership is free and available to independent contractors in the United States of all backgrounds and experience levels.

Spouse or Domestic Partner

If your spouse or domestic partner works or receives coverage through their employer, you may be eligible to join their employer-based plan. Since the employer typically pays into the plan, this may save you money and charge a lower premium.

Beyond the 401K: Investing Resources

We understand that finding quality–and affordable–health insurance is important. The good news is that there are several options for independent contractors to choose from.

Roth IRA

Like traditional IRAs, a Roth individual retirement account (IRA) is accessible to anyone with earned income. Contributions to Roth IRAs are with after-tax dollars, so they are free of tax

when you start withdrawing funds.

However, traditional IRA deposits are usually made with pretax dollars, which generally leads to a tax deduction on your contribution, and you must pay income tax when withdrawing funds from your account during retirement. Your contributions to a Roth IRA are limited to $140,000 for singles in 2021 and $144,000 in 2022. Also, the 2021 limit is $208,000 for married couples filing jointly ($214,000 in 2022).

Self-Employed 401(k)

The self-employed 401(k), also known as a solo 401(k), is another excellent plan available to self-employed workers with no employees. You will have two chances to contribute to a self-employed 401(k): as the employee first, then the employer.

As the owner, you can contribute to the plan through elective deferrals and nonelective employer contributions. You can choose to contribute elective deferrals up to 100% of the amount of compensation up the annual contribution limit.

You can also make nonelective employer contributions up to a fourth of compensation. Total contributions to an account for individuals aged 50 and over cannot exceed $61,000 for 2022 (and $58,000 for 2021).

SEP IRA

Known as a Simplified Employee Pension plan, the SEP IRA is accessible to sole proprietors and self-employed workers. Contributions may be tax-deductible, and the maximum amount that an employer can contribute to a SEP IRA is either $58,000 for 2021 ($57,000 for 2020) or 25% of eligible compensation–whichever is lower. This plan, which is usually convenient and inexpensive to maintain, works well for freelancers, independent contractors, and sole entrepreneurs.

SIMPLE IRA

Like 401(k), a Savings Incentive Match Plan for Employees (SIMPLE) IRA account is a superb choice for self-employed workers or businesses with 100 employees or fewer. As an employee, you can contribute the total amount of your compensation (up to $13,500 in 2021). You must give either a 3% matching contribution or a 2% nonelective contribution as the employer. The SIMPLE IRA also enables individuals aged 50 and over to save an extra $3,000 annually.

HSA

Another suggestion is to open a health savings account (HSA), a tax-advantaged savings account for those covered by a qualified HSA-eligible high-deductible health plan (HDHP). However, you’re not eligible for a self-employed HSA plan if you are enrolled in Medicare/Medicaid or listed as a dependent on another individual’s tax return.

HSA accounts provide many benefits to independent contractors, including tax-free growth potential, a tax deduction, and tax-free withdrawals to cover medical expenses–either immediately or after you retire. You can withdraw funds from the account without a penalty after age 65, even if you do not need the funds for medical expenses. However, like the traditional IRA, taxes will be due on earnings and contributions.

Understanding Taxes

As an independent contractor, you aren’t an employee of any company, so you will file taxes differently than you would as a W2 employee. Here are the primary differences:

Self-Employment Tax

Beyond income tax, independent contractors must also pay self-employment tax (SE tax) and file Schedule C, which indicates your loss and profit from the business. You can determine your self-employment tax through Schedule SE on Form 1040. Any income that an independent contractor earns should be reported on Schedule C, and you will pay income taxes on the entire profit.

SE tax is a Medicare and Social Security tax specifically for people who work for themselves. However, when you were an employee, your employer paid for half of the cost of the taxes. As a self-employed worker, you will be mandated to pay the whole tax yourself. This tax is comparable to Medicare and Social Security taxes that are withheld from the paycheck of most employees. The self-employment tax rate adds up to 15.3%: 2.9% for Medicare and 12.4% for Social Security.

Deductions

While it’s true that independent contractors must pay more because of self-employment taxes, you can offset much of it through business deductions. The dollar amount on which you’ll pay income taxes decreases as a result of these deductions. Business deductions for independent contractors can include home office deductions, health insurance, deductions for your telephone bill, mileage, legal expenses, rent or lease payments, and more. You can report business deductions in addition to your income on Schedule C.

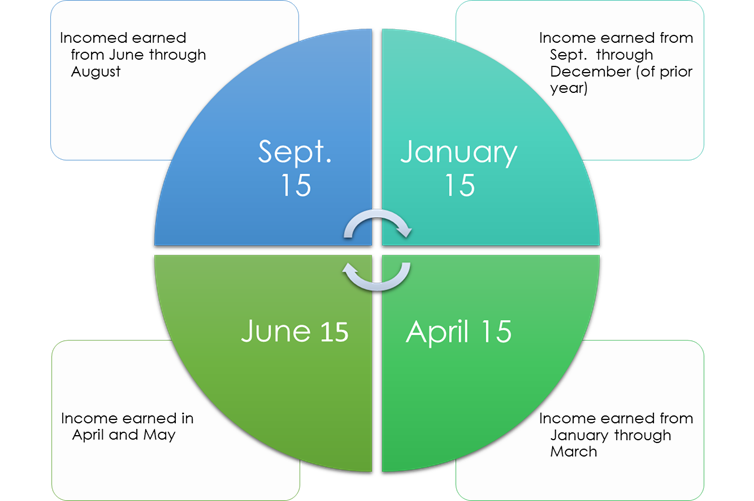

Quarterly Estimated Tax Payments

As a W2 employee, it is your employer’s responsibility to withhold income taxes from your paycheck and give it to the government. However, as an independent contractor, you will be required to regularly pay the government through quarterly estimated income tax payments during the year. These payments provide coverage for your self-employment tax and the year’s income tax liability. The quarterly federal and state tax deadlines are:

- January 15th

- April 15th

- June 15th

- September 15th

1099-MISC

As an independent contractor, you will not receive a W-2 but a 1099-MISC, which specifies the amount you were paid during the year. We suggest utilizing this information to confirm that you’re reporting all of your earned income throughout the year. However, if you made less than $600, you must still report that income amount on your Schedule C, although the payer is not required to send you a Form 1099-MISC.